GST Rates in 2022 – List of Goods and Service Tax Rates, Slab & Revision

Updated on: Nov 7th, 2022

|

7 min read

GST rates list is crucial for every Indian business and consumer to know. When the GST Council revises GST rates, it hits respective industries, trade bodies and end consumers, impacting the economy. Everyone tends to evaluate their position as a result of this change. Our HSN cum GST rates finder helps you identify the accurate and latest GST rate applicable for the product/service.

In this article, learn the meaning of GST rate and catch all the latest updates on GST rates in India 2022.

Meaning of GST Rates

GST rates refer to the percentage rates of tax imposed on the sale of goods or services under the CGST, SGST and IGST Acts. A business registered under the GST law must issue invoices with GST amounts charged on the value of supply.

The GST rates in CGST and SGST (For intra-state transactions) are approximately the same. Whereas, the GST rate in the case of IGST

(For inter-state transactions) is approximately the sum total of CGST and SGST rate.

Types of GST Rates and GST Rate structure in India

The primary GST slabs for any regular taxpayers are presently pegged at 0% (nil-rated), 5%, 12%, 18% & 28%. There are a few lesser-used GST rates such as 3% and 0.25%.

Also, the composition taxable persons must pay GST at lower or nominal rates such as 1.5% or 5% or 6% on their turnover. There is a concept of TDS and TCS under GST as well, whose rates are 2% and 1% respectively.

These are the total GST rate of IGST for interstate supply or the addition of both CGST and SGST for intrastate supply. The GST rates shall be multiplied by the assessable value of the supply to arrive at the GST amounts in a tax invoice.

Further, the GST law levies cess in addition to the above GST rates on the sale of some items such as cigarettes, tobacco, aerated water, petrol, and motor vehicles, rates widely varying from 1% to 204%.

The GST rate structure for some of the commonly-used consumable products is given in the below table. For more items, type in the item you wish to know the GST rate of by visiting our HSN code & GST rates finder.

| Tax Rates | Products | |

|---|---|---|

| 0% | Milk | Kajal |

| 0% | Eggs | Educations Services |

| 0% | Curd | Health Services |

| 0% | Lassi | Children’s Drawing & Colouring Books |

| 0% | Unpacked Foodgrains | Unbranded Atta |

| 0% | Unpacked Paneer | Unbranded Maida |

| 0% | Gur | Besan |

| 0% | Unbranded Natural Honey | Prasad |

| 0% | Fresh Vegetables | Palmyra Jaggery |

| 0% | Salt | Phool Bhari Jhadoo |

| 5% | Sugar | Packed Paneer |

| 5% | Tea | Coal |

| 5% | Edible Oils | Raisin |

| 5% | Domestic LPG | Roasted Coffee Beans |

| 5% | PDS Kerosene | Skimmed Milk Powder |

| 5% | Cashew Nuts | Footwear (< Rs.500) |

| 5% | Milk Food for Babies | Apparels (< Rs.1000) |

| 5% | Fabric | Coir Mats, Matting & Floor Covering |

| 5% | Spices | Agarbatti |

| 5% | Coal | Mishti/Mithai (Indian Sweets) |

| 5% | Life-saving drugs | Coffee (except instant) |

| 12% | Butter | Computers |

| 12% | Ghee | Processed food |

| 12% | Almonds | Mobiles |

| 12% | Fruit Juice | Preparations of Vegetables, Fruits, Nuts or other parts of Plants including Pickle Murabba, Chutney, Jam, Jelly |

| 12% | Packed Coconut Water | Umbrella |

| 18% | Hair Oil | Capital goods |

| 18% | Toothpaste | Industrial Intermediaries |

| 18% | Soap | Ice-cream |

| 18% | Pasta | Toiletries |

| 18% | Corn Flakes | Computers |

| 18% | Soups | Printers |

| 28% | Small cars (+1% or 3% cess) | High-end motorcycles (+15% cess) |

| 28% | Consumer durables such as AC and fridge | Beedis are NOT included here |

| 28% | Luxury & sin items like BMWs, cigarettes and aerated drinks (+15% cess) |

|

What are the GST rates in India 2022?

The GST Council has revised the GST rates of some key items during 2022 during its meetings. Some were done to correct the prevailing inverted tax structure whereas a few were revised for revenue augmentation. The following sections cover the summarised details of changes to GST rates in India with the new GST rates 2022.

GST Rate Changes from 18th July 2022

The government issued nine Central Tax (Rate) notifications number 03/2022 to 11/2022 on 13th July 2022. These GST rate changes will apply from 18th July 2022. Further, exemptions were withdrawn on a few daily essentials. The government notified revised rates for items that faced an inverted tax structure. Also, the taxman notified changes in the applicability of the reverse charge mechanism for certain services. Take a glimpse of the below GST rate chart revised by the notification.

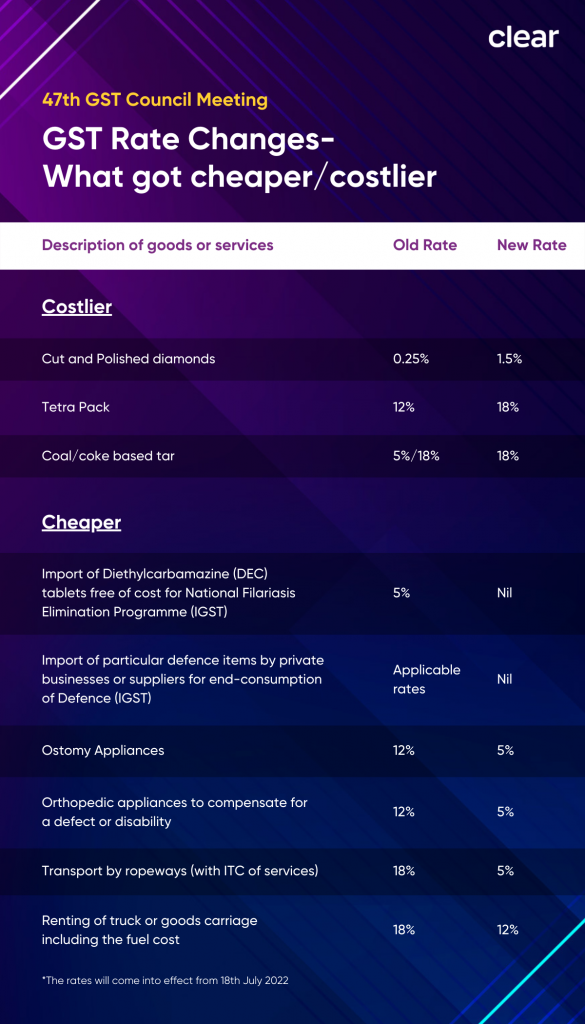

GST Rate revision in 47th GST Council Meeting

The 47th GST council meeting was held on 28th and 29th June 2022. The following decisions were taken regarding GST rates, including pruning of the exemption list and correction of the inverted tax structure.

GST rate hikes and cuts

| Description of goods or services | Old Rate | New Rate |

|---|---|---|

| What's costlier | ||

| Cut and Polished diamonds | 0.25% | 1.50% |

| Tetra Pack (Aseptic Packaging Paper) | 12% | 18% |

| Tar (From coal, or coal gasification plants, or producer gas plants and coke oven plants) | 5%/18% | 18% |

| What's cheaper | ||

| Import of tablets called Diethylcarbamazine (DEC) free of cost for National Filariasis Elimination Programme (IGST) | 5% | Nil |

| Import of particular defence items by private businesses or suppliers for end-consumption of Defence (IGST) | Applicable rates | Nil |

| Ostomy Appliances | 12% | 5% |

| Orthopedic appliances such as intraocular lens, artificial parts of the body, splints and other fracture appliances, other appliances which are worn or carried, or body implants, to compensate for a defect or disability | 12% | 5% |

| Transport of goods and passengers by ropeways (with ITC of services) | 18% | 5% |

| Renting of truck or goods carriage including the fuel cost | 18% | 12% |

| *The rates will come into effect from 18th July 2022 subject to CBIC notification | ||

Pruning of GST exemptions

| Description of goods or services | Old Rate | New Rate |

|---|---|---|

| Earlier fully exempted, now withdrawn | ||

| Maps and hydrographic or similar charts of all kinds, including atlases, wall maps, topographical plans and globes, printed | Nil | 12% |

| Cheques, lose or in book form | Nil | 18% |

| Parts of goods of heading 8801 | Nil | 18% |

| Air transportation of passengers to and from north-eastern states and Bagdogra now restricted to economy class | Nil | Condition added |

| Transportation by rail or a vessel of railway equipment and material, storage or warehousing of commodities attracting tax such as copra, nuts, spices, jaggery, cotton, etc, fumigation in a warehouse of agri produce, services by RBI, IRDA, SEBI, FSSAI, and GSTN, renting of residential dwelling to GST-registered businesses, and services by the cord blood banks for preserving stem cells | Nil | Applicable rate |

| Room rent (excluding ICU) exceeding Rs.5,000 per patient day taxed without ITC | Nil | 5% |

| Common bio-medical waste treatment facilities for treating or disposing biomedical waste shall be taxed with availability of ITC, like CETPs | Nil | 12% |

| Hotel accommodation priced up to Rs.1,000 per day | Nil | 12% |

| Training or coaching in recreational activities on arts or culture, or sports other than by individuals | Nil | Applicable rate |

| Earlier partially exempted, now withdrawn | ||

| Petroleum/ Coal bed methane | 5% | 12% |

| e-Waste | 5% | 18% |

| Scientific and technical instruments to public funded research institutes | 5% | Applicable rate |

| *The rates will come into effect from 18th July 2022 subject to CBIC notification | ||

Correction of Inverted tax structure

| Description of goods or services | Old Rate | New Rate |

|---|---|---|

| Solar water heaters and systems | 5% | 12% |

| Prepared or finished leather or chamois leather or composition leathers | 5% | 12% |

| Job work for processing of hides, skins, leather, making of leather products including footwear, and clay brick manufacturing | 5% | 12% |

| Earthwork works contracts and sub-contracts to the Central and state governments, Union Territories and local authorities | 5% | 12% |

| Pawan Chakki being air-based atta chakki, wet grinder, cleaning, sorting or grading machines for seeds and grain pulses, and milling machines or cereal making machines, etc; | 5% | 18% |

| Ink for drawing, printing, and writing | 12% | 18% |

| Knives with paper knives, cutting blades, pencil sharpeners and its blades, skimmers, cake-servers, spoons, forks, ladles, etc | 12% | 18% |

| Centrifugal pumps, submersible pumps deep tube-well turbine pumps, bicycle pumps that are power-driven mainly for handling water | 12% | 18% |

| Milking machines and dairy machinery, cleaning, sorting or grading machines and its parts for eggs, fruit or other agri produce | 12% | 18% |

| Lights and fixture, LED lamps, their metal printed circuits board | 12% | 18% |

| Marking out and drawing instruments | 12% | 18% |

| Services by foreman to chit fund | 12% | 18% |

| Works contract for railways, metro, roads, bridges, effluent treatment plant, crematorium, etc. | 12% | 18% |

| Works contract and sub-contract to the Central and state governments, local authorities for canals, dams, pipelines, plants for water supply, historical monuments, educational institutions, hospitals, etc | 12% | 18% |

| Refund of accumulated ITC for edible oils and coal is disallowed. | ||

| *The rates will come into effect from 18th July 2022 subject to CBIC notification | ||

GST Rate changes from 1st January 2022

(1) New HSN Codes from 2022

Three notifications were issued on 28th December 2021 by the CBIC to align HSN codes with HS-2022 with effect from 1st January 2022. Central Tax (Rate) notification no. 18/2021, Central Tax (Rate) notification no. 19/2021 and Central Tax (Rate) notification no. 20/2021

(2) GST rate changes to correct the inverted tax structure:

GST increased to 12% from 5% for textiles with HSN codes 51, 52, 53, 54, 55, 56, 58, 60, 63 and 64 such as woven as well as knitted fabrics, knitting, saree falls, embroidery works, curtains bed linen and home furnishings. It also includes dyeing services.

The same increase applies to footwear with HSN code 64 valued at or below Rs.1,000 per pair.

Changes were notified vide the Central Tax (Rate) notification no. 14/2021 and 15/2021 dated 18th November 2021, as recommended at the 45th GST Council meeting.

(3) e-Commerce operators to pay GST under Section 9(5) for passenger transport and restaurant services

e-Commerce operators will become liable to pay GST under Section 9(5) for the cab services, carrier services, etc provided for transportation of passengers since they are removed from the list of exemptions. This is notified by the Central Tax (Rate) notification no. 16/2021 dated 18th November 2021.

Further, the transport of passenger service included under Section 9(5) of the CGST Act will also include omnibus and other motor vehicles. Further, cloud kitchens e-commerce operators providing the supply of food will also be included under Section 9(5) and subject to GST. However, it exempts food supply services from premises having hotel accommodation where the declared tariff per unit is at or below Rs.7,500. These two are notified vide the Central Tax (Rate) notification no. 17/2021 dated 18th November 2021.

(4) Other GST rate changes

a) Exempts ‘carriages for disabled persons’ under HSN code 8713 earlier taxed at 12% by the Central Tax (Rate) notification no. 13/2021 dated 27th October 2021. Further, the same notification removed ‘in respect of Information Technology software’ from entry 452P earlier charged 18% GST.

b) Central Tax (Rate) notification no. 15/2021 dated 18th November 2021 removed ‘Governmental Authority or a Government Entity’ from serial 3 being construction services.

c) Key changes are carried out to the description of goods chargeable to GST vide the Central Tax (Rate) notification no. 18/2021 dated 28th December 2021.

d) Key changes are carried out to the description of goods exempt from GST vide the Central Tax (Rate) notification no. 19/2021 dated 28th December 2021.

e) A concessional GST rate of 12% applies to HSN code chapter 4414 instead of earlier 44140000 covering wooden frames having paintings, photos,

mirrors, etc. Also, a concessional GST rate of 12% applies to HSN code 7419 80 instead of earlier 741999 covering art ware related to brass, copper or its alloys, electroplated with nickel/silver.

GST Rate revision in 45th GST Council Meeting

The 45th GST council meeting was held on 17th September 2021 and the following decisions had been taken regarding GST rates.

These have been notified vide Central Tax (Rate) notification nos. 6, 7, 8, 9, 10 and 11/2021 dated 30th September to apply with effect from 1st October 2021.

Central Tax (Rate) notification no. 12/2021 dated 30th September 2021 grants extension to exempt the COVID-19 treating medicines up to 31st December 2021.

GST Rates reduced on Goods & Services:

| Item | Before | After |

|---|---|---|

| Import of expensive life-saving medicines such as Zolgensma, Viltepso or as recommended by a relevant government department for personal use | 12% | Nil |

| Waste unintentionally generated during the fish meal production, except for Fish Oil | Applicable rate | Nil from 1st July 2017 to 30th September 2019 |

| IGST on the goods sold at Indo-Bangladesh border haats | Applicable rate | Nil |

| Transport of goods by vessel and air from India to outside India extended up to 30th September 2022 | Nil | Nil |

| Granting of National Permit to goods carriages on a fee payment | 18% | Nil |

| Skill training programmes where the state/central government funds expenditure equal to or more than 75% | 18% | Nil |

| Services on AFC Women's Asia Cup to be held in 2022 | 18% | Nil |

| ‘Keytruda’ drug for the treatment of cancer | 12% | 5% |

| Biodiesel, sold to the oil marketing companies for blending it with diesel | 12% | 5% |

| Fortified Rice Kernels for the Integrated Child Development Services Scheme, etc | 18% | 5% |

| Retro fitment kits in vehicles for the disabled | Applicable rate | 5% |

*With effect from 1st October 2021 subject to the CBIC notification

GST Rates increased on Goods & Services:

| Item | Before | After |

|---|---|---|

| Polyurethanes and other plastics waste and scrap | 5% | 18% |

| Cartons, bags, boxes, packing containers made out of paper, etc | 12/18% | 18% |

| Papers such as cards, catalogue, printed material Under Chapter 49 | 12% | 18% |

| Licensing, broadcasting and showing original films, Radio Television programmes, sound recordings | 12% | 18% |

| Printing and reproduction of recorded media being the publisher’s content | 12% | 18% |

*With effect from 1st October 2021 subject to the CBIC notification

GST rate corrections for inverted tax structure:

| Item | Before | After |

|---|---|---|

| Specified Renewable Energy Devices and parts | 5% | 12% |

| Ores and metal concentrates | 5% | 18% |

| All kinds of pens | 12/18% | 18% |

| Railway parts, locomotives and goods in Chapter 86 | 12% | 18% |

*With effect from 1st October 2021 subject to the CBIC notification

GST Rate revision in 44th GST Council Meeting

The 44th GST council meeting was held on 12th June 2021 and the following decisions had been taken regarding GST rates effective up to 30th September 2021.

These were notified vide the Central Tax(Rate) notification no. 04/2021 and 05/2021 dated 14th June 2021.

Medicines required for COVID-19 & Black Fungus treatment:

| Items | Old rate | Proposed rate |

|---|---|---|

| Tocilizumab | 5% | Nil |

| Amphotericin-B | 5% | Nil |

| Remedesivir | 12% | 5% |

| Anti-coagulants like Heparin | 12% | 5% |

| Any other drug (recommended by the Ministry of Health and Family Welfare (MoHFW) and the Dept. of Pharma (DoP) for Covid-19 treatment) | Existing rate | 5% |

Medical equipment required for COVID treatment:

| Items | Old rate | Proposed rate |

|---|---|---|

| Medical Grade Oxygen | 12% | 5% |

| Oxygen concentrators/ generators (which include personal imports) | 12% | 5% |

| Ventilators and ventilator masks/ cannula/ helmets | 12% | 5% |

| BiPaP machine | 12% | 5% |

| High flow nasal cannula device | 12% | 5% |

| Pulse oximeters | 12% | 5% |

COVID-19 testing kits and items utilised for the prevention of COVID-19:

| Items | Products Resources & Guides GST Resources ITR Resources Mutual Fund Resources Tools TRENDING MUTUAL FUNDS ICICI Prudential Technology Fund Direct Plan Growth Tata Digital India Fund Direct Growth Axis Bluechip Fund Growth ICICI Prudential Technology Fund Growth Aditya Birla Sun Life Tax Relief 96 Growth Aditya Birla Sun Life Digital India Fund Direct Plan Growth Quant Tax Plan Growth Option Direct Plan SBI Technology Opportunities Fund Direct Growth Axis Long Term Equity Fund Growth TOP AMCS STOCK MARKETS Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India. Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing. CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law. Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone. Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India Cleartax is a product by Defmacro Software Pvt. Ltd. ISO 27001 Data Center SSL Certified Site 128-bit encryption |

|---|